-

The Raises

One thing that never hit me about dividend growth investing versus income investing was the raises you get throughout the year. Solid companies that have been paying out and raising dividends for 25 to 50 years tend to continue doing so. I mean I understood it on a cursory level, but I didn’t really intuit…

-

The Half Way Point

I’m half way there. Over $50 dollars a month in dividends. Passive income. I wanted to be sure since dividends for funds can often change month to month, but I feel pretty confident in saying I have reached the half way point toward my goal of earning $100 dollars a month in dividends. I honestly…

-

The Guarantees

There are no guarantees in life. This is especially true in the stock market. But things are finally clicking. If you want to grow your money, the best shot you have right now is to invest it in the S&P 500 for 30 years and pile in as much capital as you can. If you…

-

The Quarterly Check In

Wow. Already three months into the year. So far I’m on track to hit my goals, but only just. I need to hit $50 dollars a month in dividends and $10,000 total invested by the end of April. I think I can do it, but as of right now it will be close. I may…

2024 GOALS AND MILESTONES

| $40/month from dividends Completed 26 February 2024 |

| $7,500 total invested Completed 12 February 2024 |

| $50/month from dividends Completed 8 April 2024 |

| $10,000 total invested Completed 8 April 2024 |

| $60/month from dividends |

| $15,000 total invested |

| $70/month from dividends |

| $3,000 earned trading stocks Completed 3 April 2024 |

| $2,000 earned completing surveys |

| $1,000 earned churning |

ARCHIVES

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

CURATED RESOURCES

Dividend Diplomats

Two 30 something’s blogging about investing, frugality, passive income and reinvesting dividends for financial freedom.

Dividend Growth Investor

A long term buy and hold investor who focuses on dividend growth stocks.

Doctor Of Credit

Bank account and credit card bonuses.

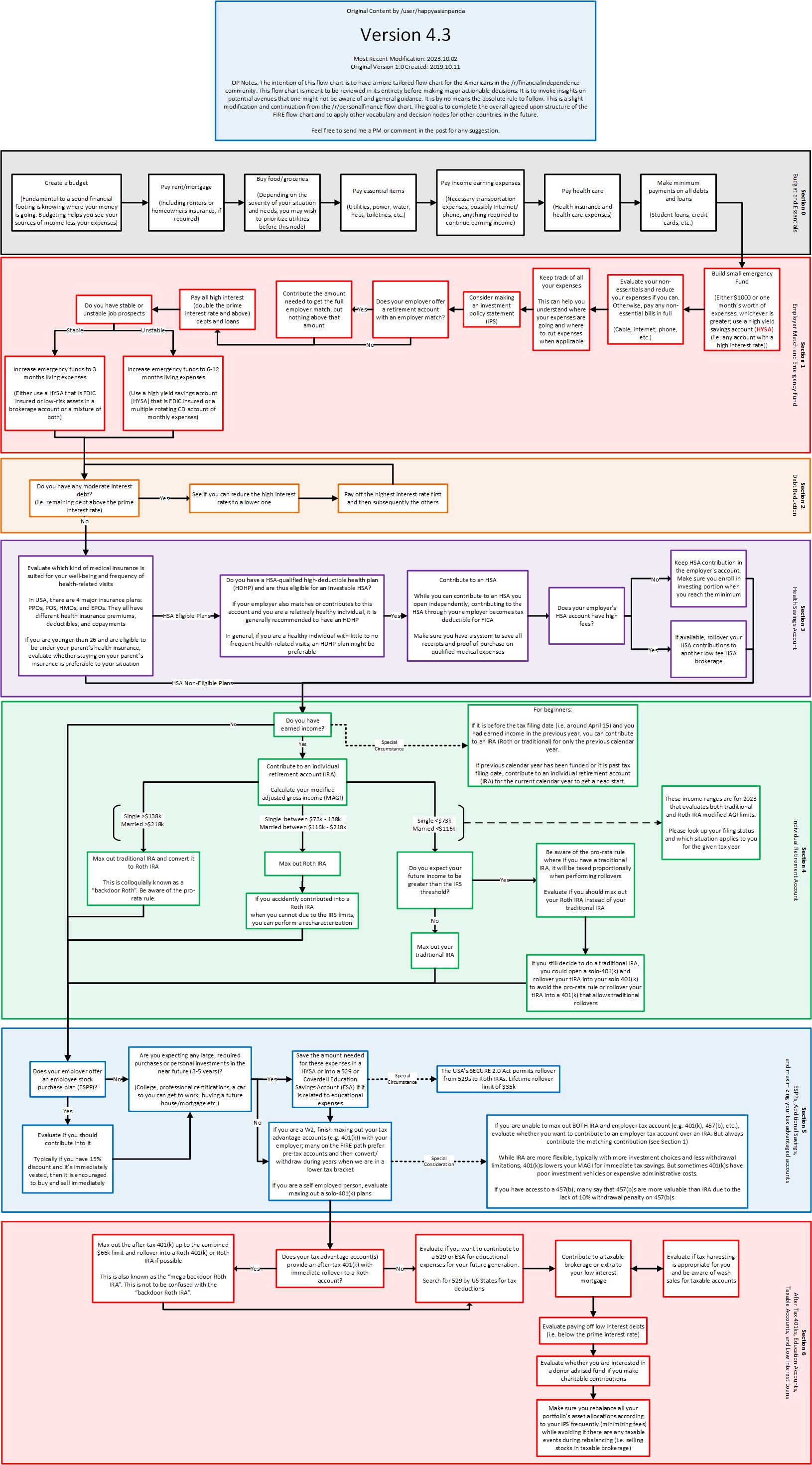

Financial Independence Flow Chart

A good, general guide for how to allocate additional savings.

Source: r/financialindependence

r/Beermoney

A community for people to discuss online money-making opportunities.

{kind=link}